Africa’s $90 Billion Debt Wall Meets a $115 Oil Shock — and Oil Exporters Are Seizing the Moment

Africa's $90 billion debt wall collides with a $115 oil shock — and Angola's historic $2.5 billion Eurobond shows oil exporters are turning crisis into opportunity while importers face a narrowing corridor.

Issue 1 | March 30, 2026 | African Capital Markets Brief

Executive Insight

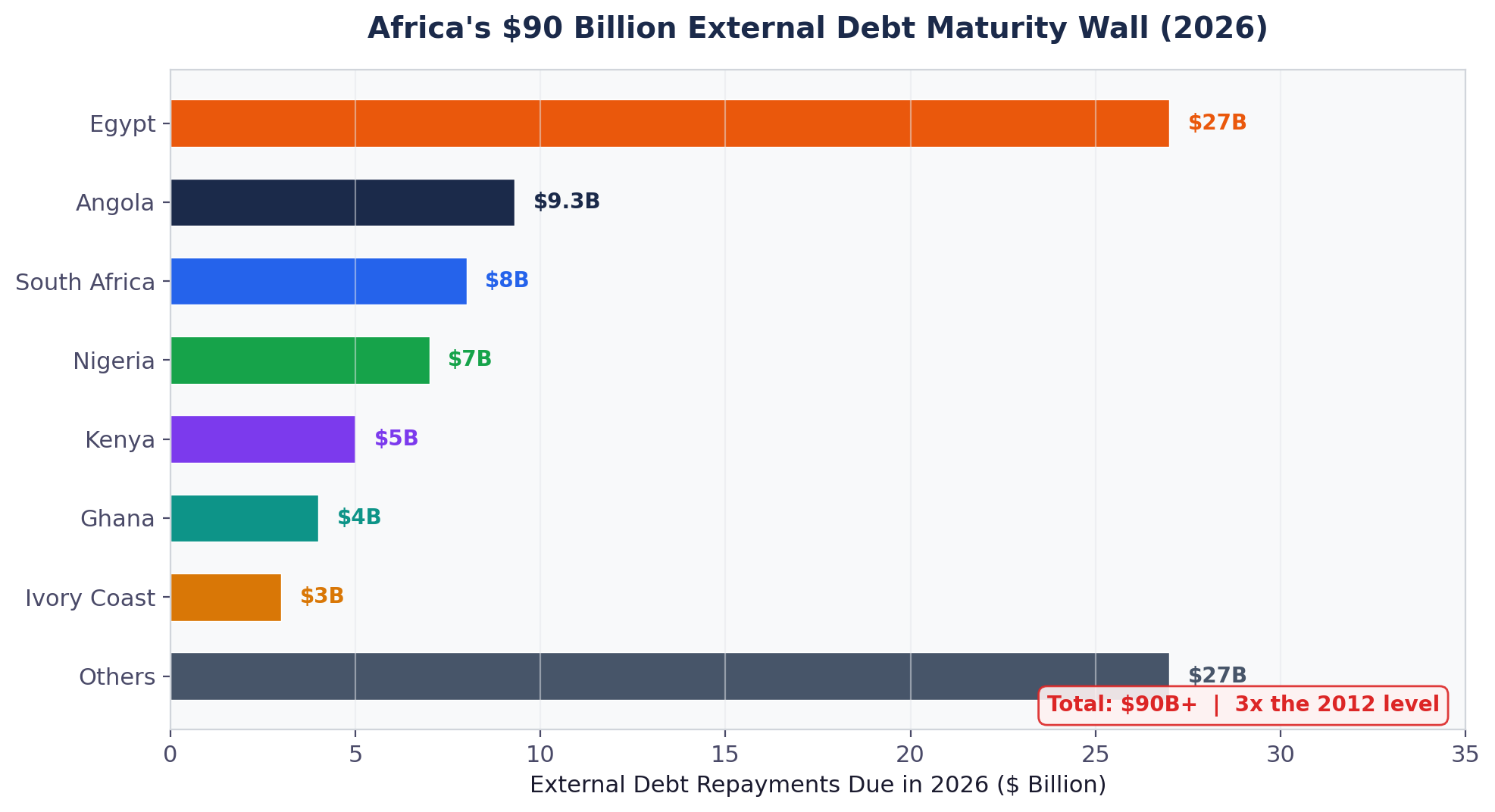

African sovereigns face more than $90 billion in external hard-currency debt repayments this year — three times the level in 2012 — just as the Strait of Hormuz closure has driven Brent crude from $77 to $115 per barrel in a single month. This oil shock has split the continent's sovereign debt story in two. For oil importers like Egypt, Kenya, and Ghana, rising energy costs are widening current-account deficits and pushing up borrowing costs at exactly the wrong time. For oil exporters — Angola, Nigeria, Gabon, and the Republic of Congo — the windfall is transformative. Angola's landmark $2.5 billion Eurobond on March 24, the first emerging-market sovereign issuance since the Iran war began, is the clearest signal yet that petrodollar-backed credit is open for business while the rest of the market remains frozen.

Key Data Snapshot

- Africa's 2026 debt wall: $90 billion+ in external repayments; Egypt leads at $27 billion, Angola at $9.3 billion

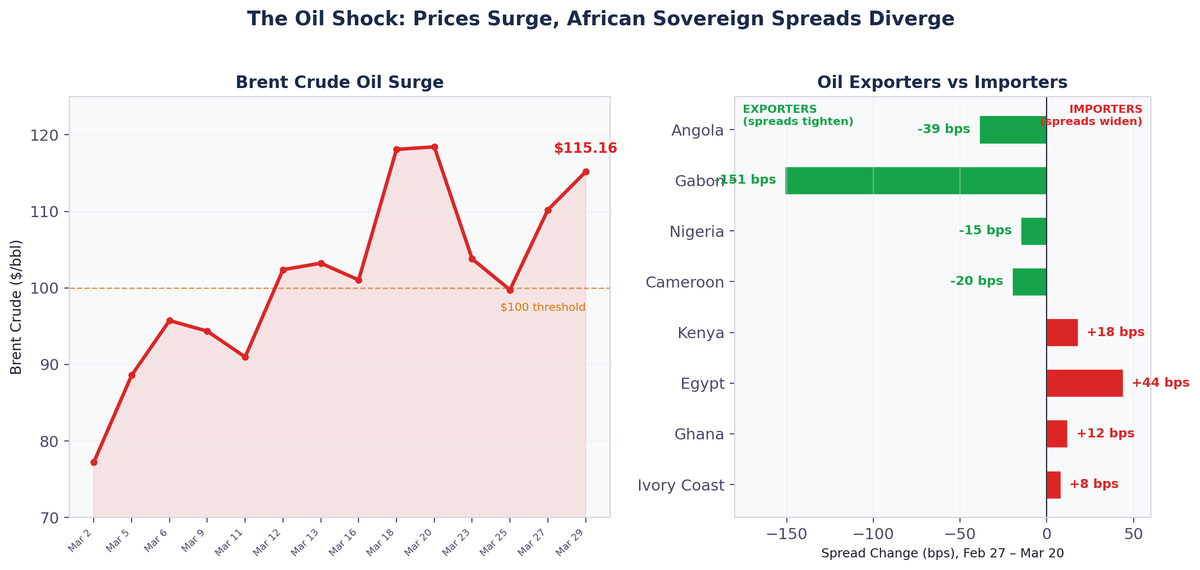

- Brent crude: $115.16/bbl (March 29) — up 49% month-on-month; Strait of Hormuz transit down 95%

- Angola Eurobond: $2.5 billion raised on March 24 at 9.25% (7-year) and 9.8% (11-year); $5.2 billion in demand — the first EM issuance since the Iran war began

- Exporter-importer spread gap: Angola spreads narrowed 39 bps; Gabon narrowed 151 bps. Egypt widened 44 bps; Kenya widened 18 bps

- Q1 2026 SSA Eurobonds: $5.95 billion issued — a 13-year record — but the primary window froze in mid-March

- Fed funds rate: Held at 3.50–3.75% (March 18); only one cut projected for 2026

The Oil Shock Splits Africa's Debt Story in Two

When IRGC forces declared the Strait of Hormuz "closed" on March 2, roughly 20% of global oil supply was cut from transit. Brent crude surged from $77.24 to an intraday peak of $118.42 on March 20, settling at $115.16 by month-end. For a continent where sovereign debt repayment capacity is tightly linked to commodity revenues, the impact is profound — but asymmetric.

Between February 27 and March 20, bond spreads for oil-exporting African sovereigns tightened significantly. Gabon's spread compressed by 151 basis points — the largest improvement among all developing countries tracked by J.P. Morgan. Angola narrowed 39 bps to 504 bps. Nigeria and Cameroon followed suit. The market is pricing a simple but powerful thesis: higher oil revenues mean stronger repayment capacity and reduced refinancing risk.

For oil importers, the story reverses. Egypt's spread widened 44 basis points as the pound fell 12% in March to record lows above 53/$, compounded by a 52% year-on-year drop in Suez Canal revenues. Kenya's 10-year Eurobond yield jumped 63 basis points in a single week as roughly 20% of fuel stations reported shortages. South Africa's rand weakened 2.7%, with the SARB explicitly modelling scenarios that could require rate hikes.

Bank of America's research note of March 21 put it plainly: "Angola and Nigeria emerge as the largest beneficiaries: both show positive current-account effects and record positive fiscal impacts." The removal of costly fuel subsidies across several exporters, BofA noted, means this cycle's windfall flows more directly to sovereign balance sheets than in previous oil booms.

Angola's $2.5 Billion Eurobond: The Oil Exporter's Moment

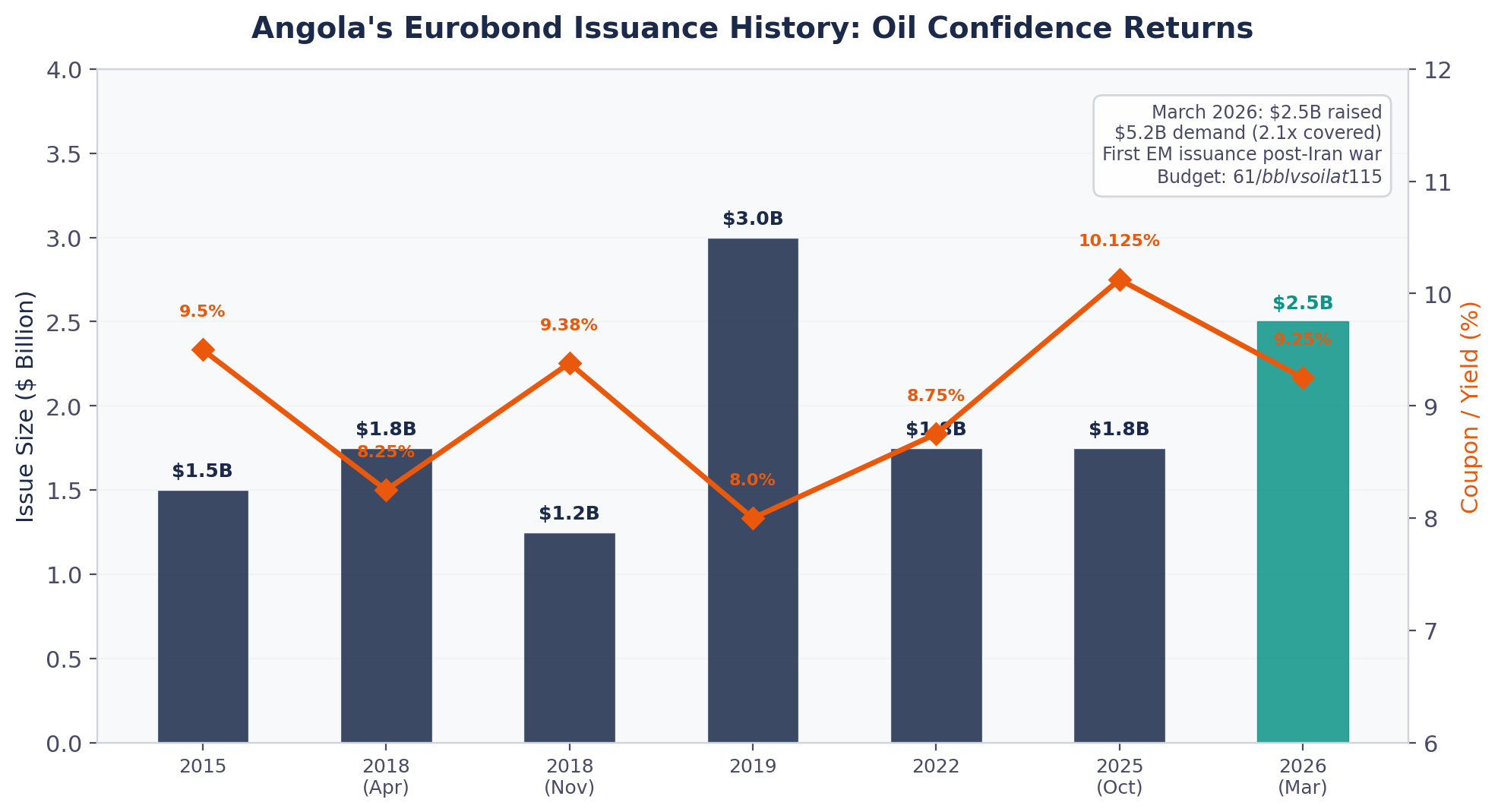

Angola's March 24 Eurobond issuance is the defining capital markets event of the period — and a case study in how oil-exporter credit operates during an energy shock.

The deal was structured as a dual-tranche issuance: $1.5 billion at 9.25% with a seven-year maturity, and $1 billion at 9.8% with an eleven-year maturity. Angola had targeted $2 billion but upsized to $2.5 billion after demand reached $5.2 billion — more than double the target. State Minister for Economic Coordination Jose de Lima Massano called it "historic," noting it was "the first sovereign debt issuance by emerging countries since the conflict broke out in the Middle East."

Three aspects make this issuance particularly significant:

First, the pricing improved. Angola secured lower yields than its October 2025 issuance (which priced at 10.125%), despite the Iran war and global risk-off environment. The 7-year tranche at 9.25% represents roughly 90 basis points of tightening from the previous benchmark. This is a market explicitly rewarding an oil exporter during an oil shock.

Second, the proceeds address structural vulnerability. Angola's 2026 debt service totals $16.2 billion — nearly 46% of its entire budget. External debt service alone is $9.3 billion. Of the $2.5 billion raised, $500 million will fund a buyback of the outstanding $1.75 billion 8.25% notes due 2028, actively managing the maturity profile. The remainder addresses budget financing and the clearance of arrears to domestic service providers.

Third, the budget arithmetic is transformative. Angola's 2026 budget assumes oil at $61 per barrel. With Brent at $115, every barrel sold generates nearly double the budgeted revenue. Angola produces approximately 1.1 million barrels per day. The implied windfall — even accounting for production-sharing agreements and operational costs — could amount to several billion dollars of additional fiscal space over the year, fundamentally changing the country's debt service trajectory.

The Sovereign Debt Wall: Who Faces It, Who Can Climb It

S&P Global Ratings estimated on March 17 that African sovereigns will borrow $155 billion commercially in 2026, with total sovereign commercial debt exceeding $1.2 trillion by year-end. The average funding cost declined roughly 100 basis points in 2025 to 7.7%, but the current market freeze threatens to reverse that for anyone needing to access the window in Q2.

The $90 billion maturity wall is not equally distributed. Egypt faces $27 billion in external repayments — the largest on the continent — at a moment when its primary revenue source (Suez Canal tolls) is collapsing and its currency is under severe pressure. Angola's $9.3 billion in external debt service, by contrast, is now backstopped by an oil price nearly double its budget assumption and a freshly executed $2.5 billion Eurobond that signals market access remains open.

Sub-Saharan Eurobond issuance had surged to $5.95 billion in January–February 2026 — the strongest start since 2013. Kenya raised $2.25 billion, Ivory Coast $1.3 billion, Republic of Congo $700 million, Cameroon $750 million, and Benin approximately $500 million. But the Iran war froze the primary window for most issuers from mid-March onward. Angola broke through that freeze; few others are positioned to follow.

Nigeria's Banking Transformation Reinforces the Exporter Advantage

Nigeria's March 31 bank recapitalisation deadline adds a structural dimension to the exporter story. Of 37 licensed banks, 32–34 have met new minimum capital requirements, with ₦4.61 trillion in new capital raised — 27% from foreign investors. Combined market capitalisation of 13 listed banks surged from ₦8.08 trillion to ₦20.83 trillion during the exercise.

For Nigeria, Africa's largest economy and a major oil exporter with a 2026 budget benchmarked at $60–65/bbl, the recapitalisation creates a banking system better equipped to intermediate the oil windfall domestically. The CBN's new Risk-Based Capital stress testing directive, effective April 1, signals regulatory intent to ensure this capital is real and resilient.

Monetary Policy and FX: The Oil Dividend in Action

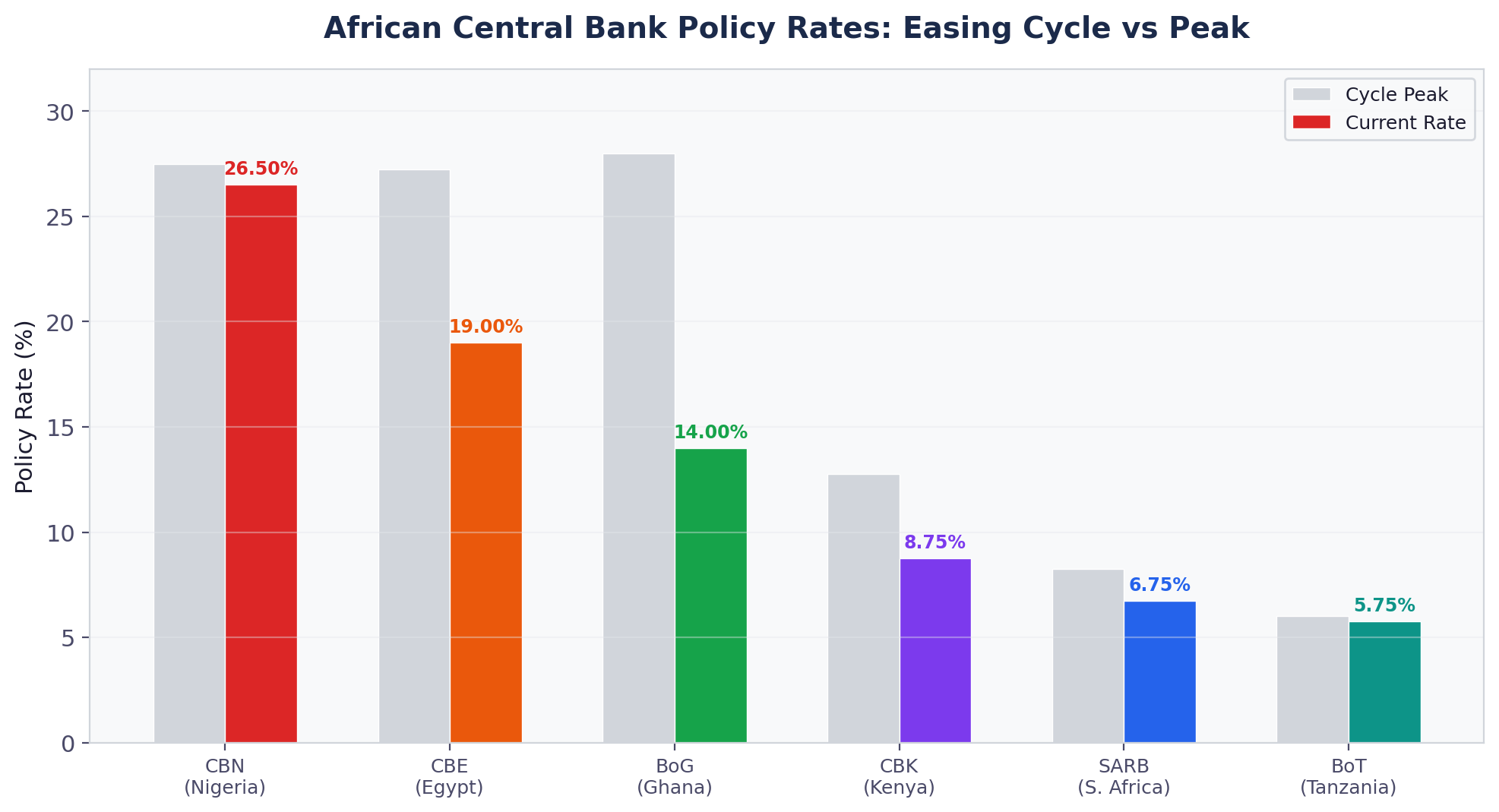

The oil shock's impact on monetary policy further reinforces the exporter-importer divergence. Most African central banks remain in easing mode: Ghana's Bank of Ghana cut 150 bps to 14% on March 18 (with inflation at just 3.3%), Nigeria's CBN cut 50 bps to 26.5%, Egypt's CBE is at 19% after 725 bps of cuts from peak, and Kenya's CBK has delivered ten consecutive reductions to 8.75%.

The SARB stands apart, holding at 6.75% and explicitly warning of potential hikes. Governor Kganyago modelled two scenarios: a two-month war pushing inflation above 4% (one hike), and a protracted conflict driving inflation past 5% (several hikes). South Africa's CPI at 3.0% is precisely on target, but fuel inflation is expected to exceed 18% in Q2.

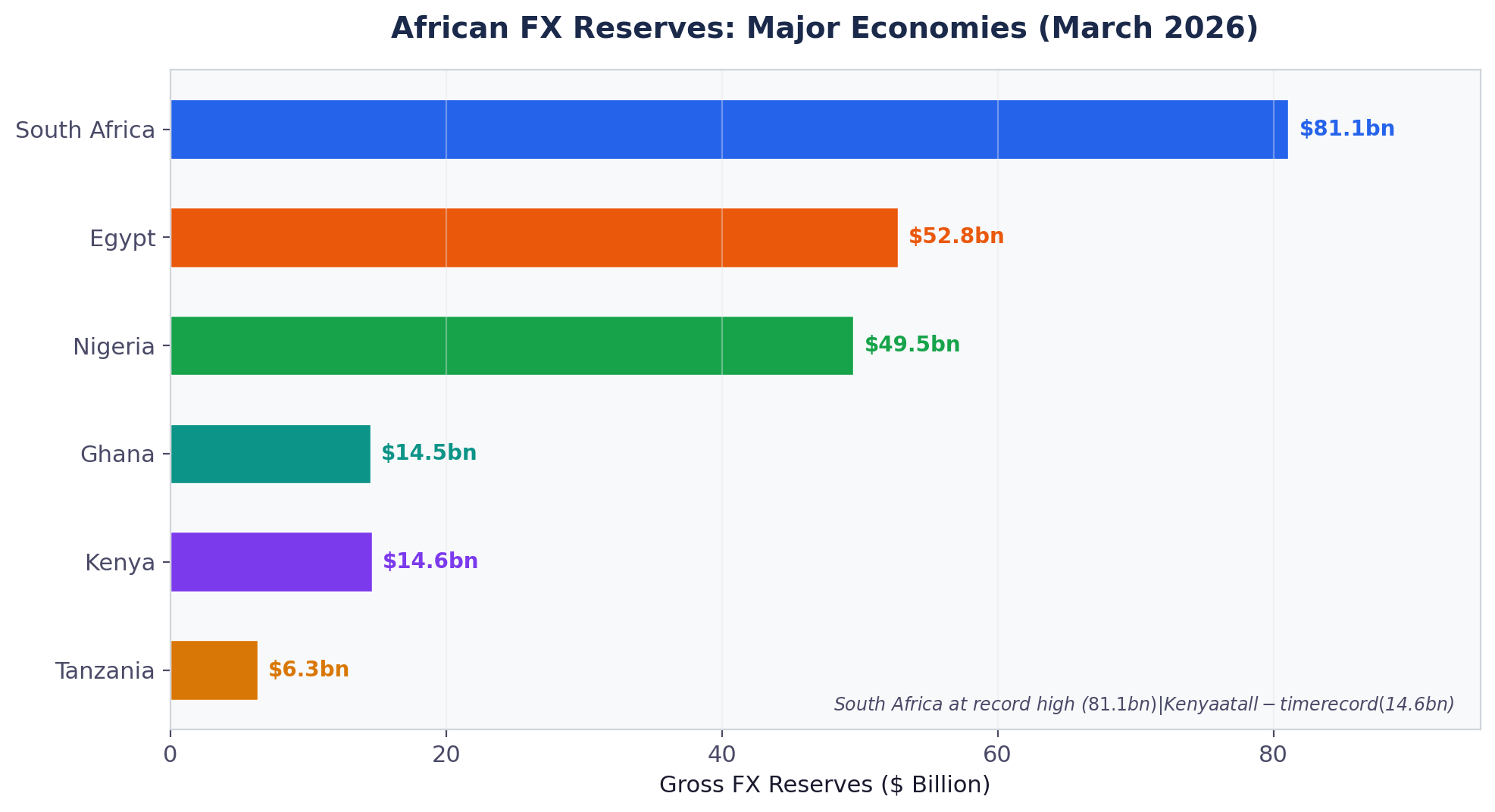

On the FX front, Nigeria's gross reserves at $49.53 billion and the naira's parallel-market premium narrowing to just 1.4–2.5% (from 30–50%+ historically) reflect the structural improvement that oil revenues and FX reform have delivered. South Africa's reserves hit a record $81.06 billion. Kenya, bolstered by Eurobond proceeds, reached an all-time high of $14.6 billion.

Forward Outlook

The April 13–18 IMF/World Bank Spring Meetings will deliver the first growth forecasts incorporating the Iran oil shock. Pre-shock consensus pegged sub-Saharan growth at 4.0–4.4% for 2026; material downward revisions for oil importers are likely.

Key dates: Nigeria bank stress test reports (April 30), CBK rate decision (April 8), Ghana 7-year bond pricing (April 1), DRC Eurobond timeline (pushed to H1 end), and the AGOA eligibility review (imminent).

The thesis is straightforward: Africa's $90 billion debt wall becomes manageable or punishing depending on which side of the oil trade a sovereign sits. Angola has demonstrated that oil exporters can not only service their debts but can actively improve their borrowing terms during a crisis. Egypt, Kenya, and other importers face a narrowing corridor of higher costs, weaker currencies, and tighter external financing. The Iran war has not created this structural divide — but it has accelerated it dramatically.

African Capital Markets Brief

Data as of March 30, 2026

Sources: S&P Global, IMF, Federal Reserve, J.P. Morgan, BofA, Fitch, Angola Finance Ministry, CBN, SARB, BoG, CBK, CBE, Bloomberg, Reuters

© 2026 African Capital Markets Brief. All rights reserved.